Should You Do SIP or Not? A Complete Guide for Beginners and Long-Term Investors

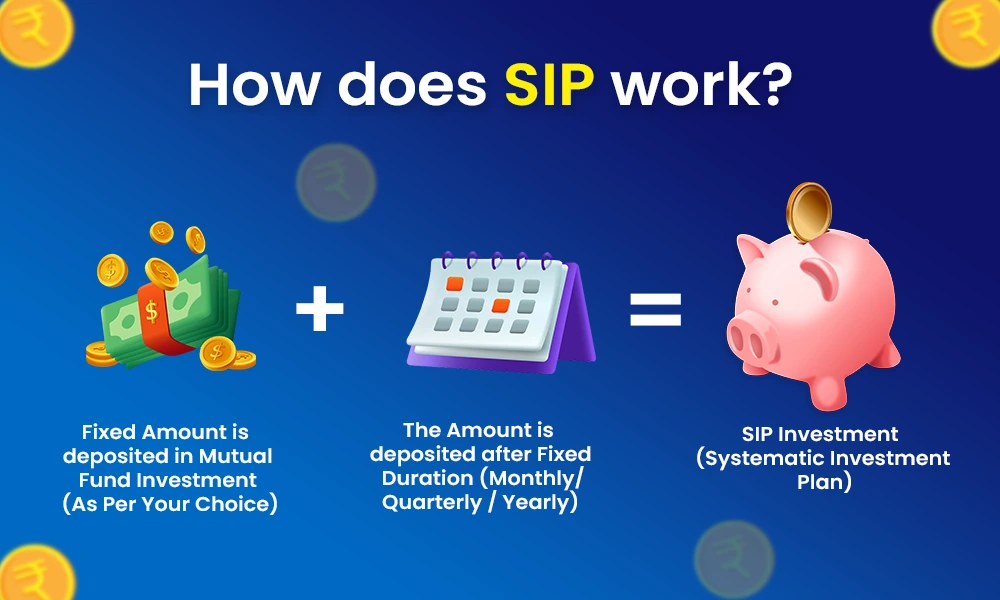

In today’s fast-changing financial world, everyone wants to grow their money. Bank fixed deposits no longer give high returns, inflation is rising, and people are constantly searching for smart investment options. One term you may have heard very often is SIP. But the big question is:Should you do SIP or not?This blog will give you a clear, honest, and beginner-friendly answer. We will discuss what SIP is, how it works, its advantages, disadvantages, myths, risks, and whether SIP is right for you or not.What Is SIP?SIP stands for Systematic Investment Plan. It is a method of investing money regularly (monthly, quarterly, or weekly) into mutual funds.Instead of investing a large amount at once, you invest a fixed small amount at regular intervals. This amount is automatically deducted from your bank account.For example:You invest $20 or ₹1,000 per monthThe money goes into a mutual fundOver time, your investment grows with the marketSIP is popular because it is simple, disciplined, and suitable for beginners.How Does SIP Work?SIP works on two powerful principles:1. Rupee Cost AveragingWhen markets go up, you buy fewer units.When markets go down, you buy more units.This balances the cost of your investment over time and reduces risk.2. Power of CompoundingYour money earns returns, and then returns start earning returns. Over a long period, this creates massive wealth.Example: If you invest ₹5,000 per month for 20 years at an average return of 12%:Total investment: ₹12,00,000Final value: Around ₹50–60 lakhsThis is the magic of SIP.Types of SIPThere are different types of SIPs available:1. Regular SIPYou invest a fixed amount every month.2. Step-Up SIPYour SIP amount increases every year (for example, 10% annually).3. Flexible SIPYou can increase or decrease the amount based on your income.4. Perpetual SIPNo fixed end date; it continues until you stop it.Why SIP Is So Popular?SIP has become popular because it fits perfectly with modern life. You don’t need financial expertise, large capital, or market timing skills.Anyone can start SIP:StudentsSalaried employeesSmall business ownersHousewivesFreelancersAdvantages of SIP (Why You Should Do SIP)Let’s understand why SIP is considered one of the best investment options.1. Discipline in InvestmentSIP forces you to invest regularly. This builds a strong financial habit.2. Affordable for EveryoneYou can start SIP with as low as ₹500 or $10 per month.3. No Need to Time the MarketMarket timing is difficult even for experts. SIP removes this stress.4. Long-Term Wealth CreationSIP is ideal for long-term goals like:RetirementChild educationBuying a houseFinancial freedom5. FlexibilityYou can:Pause SIPStop SIPIncrease or decrease amount6. Suitable for BeginnersEven if you have zero knowledge of stock markets, SIP is safe and easy.Disadvantages of SIP (Why You Should Think Before Doing SIP)SIP is not perfect. You should also know its limitations.1. No Guaranteed ReturnsSIP is linked to the market. Returns are not fixed.2. Requires PatienceSIP is not a get-rich-quick scheme. You need time (10–20 years).3. Market RiskIn the short term, markets can fall, and your portfolio may show losses.4. Wrong Fund Selection Can HurtIf you choose poor mutual funds, SIP returns may be low.Common Myths About SIPMyth 1: SIP Is Risk-Free❌ False. SIP reduces risk but does not eliminate it.Myth 2: SIP Always Gives High Returns❌ Returns depend on market performance and fund quality.Myth 3: SIP Is Only for Salaried People❌ Anyone with regular or irregular income can do SIP.Myth 4: SIP Is Better Than Lump Sum Always❌ Both have their place. SIP is better for long-term discipline.SIP vs Lump Sum InvestmentFeatureSIPLump SumInvestment StyleMonthlyOne-timeRiskLowerHigherMarket TimingNot requiredRequiredBest ForBeginnersExperienced investorsFor most people, SIP is better than lump sum.Who Should Do SIP?You should do SIP if:✔ You are a beginner✔ You have a regular income✔ You want long-term wealth✔ You don’t understand market timing✔ You want disciplined investingWho Should NOT Do SIP?You may avoid SIP if:❌ You need money in the short term❌ You want guaranteed returns❌ You cannot tolerate market ups and downs❌ You expect quick profitsIs SIP Safe?SIP is as safe as mutual funds. Mutual funds are regulated by authorities like SEBI

(in India) and similar regulators globally.However:SIP is not bank FDCapital is not guaranteedLong-term investment reduces risk significantlyHow Much Should You Invest in SIP?A simple rule:Invest 10–30% of your monthly incomeStart small and increase gradually.Example:Income: ₹20,000/monthSIP: ₹2,000–₹5,000/monthHow Long Should You Continue SIP?Minimum recommended duration:5 years (better)10–20 years (best)The longer you stay invested, the better your returns.Best Mutual Funds for SIP (General Categories)You can choose funds based on your risk appetite:Low RiskDebt FundsLarge Cap FundsMedium RiskBalanced / Hybrid FundsIndex FundsHigh RiskMid Cap FundsSmall Cap FundsFor beginners, Index Funds or Large Cap Funds are recommended.SIP During Market Crash – Should You Continue?Yes, absolutely.Market crashes are the best time for SIP investors because:You buy more units at low pricesLong-term returns improveStopping SIP during market fall is the biggest mistake investors make.SIP for Retirement PlanningSIP is one of the best tools for retirement planning.If you start early:Small amountLong durationHuge corpusStarting SIP at age 25 is much better than starting at 40.Tax Benefits of SIPTax benefits depend on the fund type:ELSS SIP offers tax deduction under certain lawsLong-term capital gains tax may applyAlways check current tax rules.Real-Life Example of SIP Wealth CreationPerson A:Starts SIP at age 25Invests ₹5,000/monthStops at age 45Person B:Starts SIP at age 35Invests ₹5,000/monthStops at age 55Person A invests less money but ends with more wealth because of early start and compounding.Should You Do SIP or Not? Final VerdictYES, you should do SIP if:You want long-term financial growthYou are disciplinedYou understand that markets fluctuateNO, you should not do SIP if:You want short-term profitsYou cannot tolerate lossesYou want guaranteed returns